Preparing your house for sale (LEGAL) Top 13 things you need BEFORE you put your house up for sale. Below is a list of the 13 absolutely vital things that you will need BEFORE you put your house or apartment up for sale, especially if you are going to buy another property using the proceeds of the sale

Preparing your house for sale (LEGAL)

Top 13 things you need BEFORE you put your house up for sale.

Below is a list of the 13 absolutely vital things that you will need BEFORE you put your house or apartment up for sale, especially if you are going to buy another property using the proceeds of the sale.

1. Appointing a Solicitor

You will need to have a solicitor in place to sell your property. Solicitor’s fees can vary a lot and may be either a percentage of the price of the property, or a flat fee. You will usually be charged additional fees for services like phone calls, postage, search fees and registering deeds, so, before you choose a solicitor get several written quotes that include their professional fees and other costs.

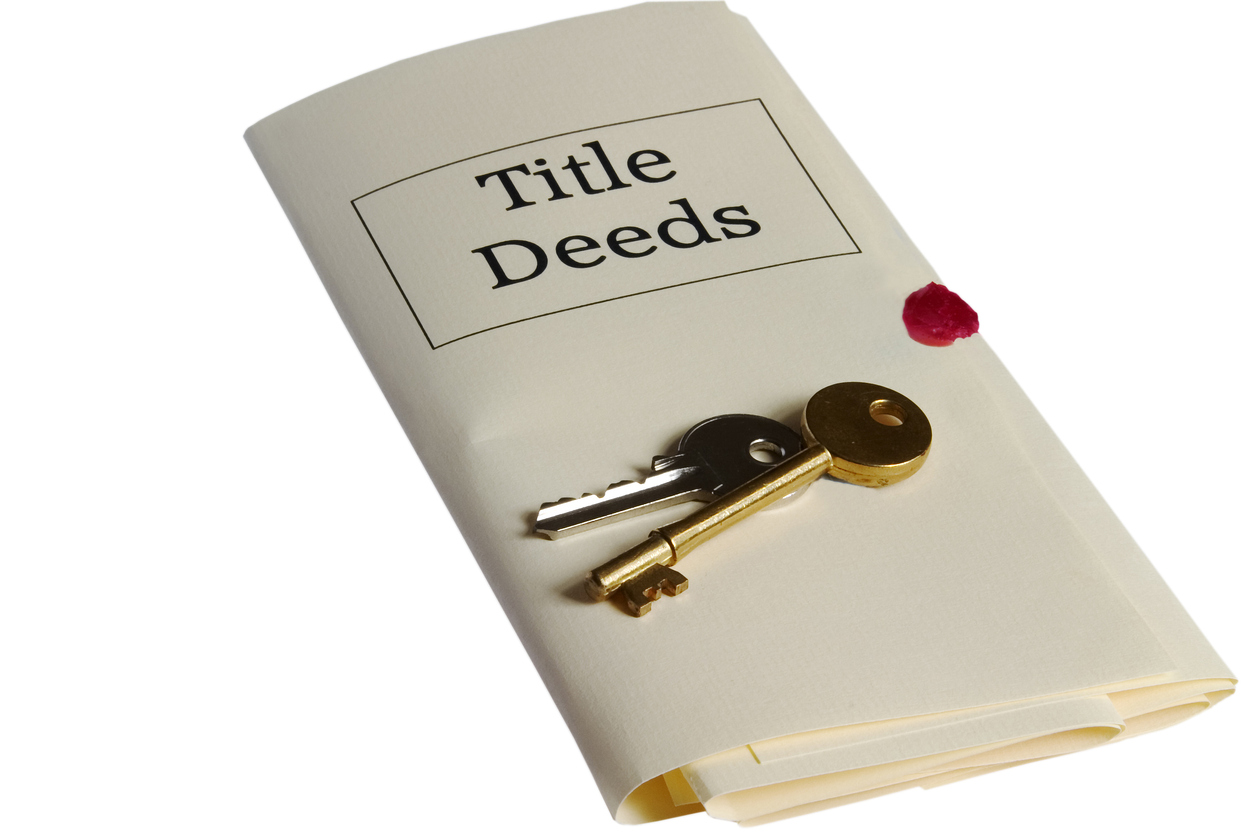

2. Instruct your Solicitor to draw down the Title Deeds from your bank

If you have a mortgage, your solicitor must request your title deeds from your lender. It is from your Title Deeds that your solicitor with draft the contract for sale. It can take between four and eight weeks for your lender to issue the deeds. To avoid unnecessary delays, instruct your solicitor to request the deeds as soon as possible. If you don’t have a mortgage, give your title deeds to your solicitor. Once the solicitor has the title deeds, he or she will investigate the title and see if they need to apply for any documents in order to complete the sale.

3. Identity Documentation

Provide your solicitor with a copy of your photo ID and a utility bill for Anti-Money Laundering (AML)purposes.

4. Pay your Local Property Tax (LPT) and provide your solicitor with the receipt.

Arranging your payment online: The easiest way to pay your LPT charge is online. This gives you a wide range of secure payment options:

Single payment in full

Debit or credit card

Annual Debit Instruction(ADI)

One-off cash payment through an approved Payment Service Provider.

Phased payments (instalments) to spread your payments throughout 2022

Monthly direct debit

Weekly or monthly cash payments through an approved Payment Service Provider

Deduction at source (from your salary, wages, occupational pension, Department of Social Protection payment or Department of Agriculture, Food and the Marine payment)

For those who chose the ADI option, the payment was deducted from their bank account by 21 March 2022.

If you are liable for Local Property Tax (LPT) on more than one property, you are required to arrange your payment for LPT through one of the online payment options.

Arranging your payment using your paper LPT Return

If you submit your LPT Return using the paper Form LPT1, instead of submitting it online, your payment options are limited to:

· single payment in full

· cheque payment

· one-off cash payment through an approved Payment Service Provider.

· phased payments (instalments) to spread your payments throughout 2022:

· weekly or monthly cash payments through an approved Payment Service Provider

· deduction at source (from your salary, wages, occupational pension, Department of Social Protection payment or Department of Agriculture, Food and the Marine payment)

Even if you choose to submit your valuation on the paper LPT Return, you can still arrange your payment online through the LPT online service.

5. Obtain a Building Energy Rating Certificate (BER)

A BER certificate is required if you are advertising a home for sale or rent, or before a new home is occupied for the first time. It shows how energy efficient your home is and checks energy use for space heating, water heating, ventilation, and lighting. Your home is rated between A and G, with A-rated homes being the most energy efficient. You will need to have this certificate before we advertise your property. We at Hogan Estates have a number of trusted BER assessors that we can recommend to carryout an assessment on your property.

6. If your property is a RENTAL PROPERTY, you need to pay the NPPR and give the receipt to your solicitor.

Non-Principal Private Residences.

The charge on non-principal private residences (NPPR) was introduced in 2009 under the Local Government (Charges Act 2009, as amended. The charge is payable by the owners of private rented accommodation, holiday homes and other non-principal private residences.

7. Water Rates Certificate of Discharge

The onus is on the owner of the property to provide to his or her solicitor a certificate/statement from Irish Water confirming that all water charges are paid. This could prove difficult if the property is rented as it is the occupier of the property, the tenant, who is responsible for this utility. If the owner fails to do this, the solicitor must contact Irish Water directly and request the information and certificate directly from Irish Water. If Irish Water then confirms that water charges are outstanding and owed, it will then become the obligation of that solicitor to withhold the arrears from the proceeds of sale and pay it to Irish Water within20 working days of completing the sale.

8. Permission to Sell from the Bank (if you have a mortgage and you are in Negative equity)

Negative equity can mean selling your home for less than the value of the mortgage you took out to buy it. This is because you’ll have an outstanding amount of money on the mortgage that you must pay back after the sale.

Selling your house while in negative equity should not be taken lightly. It should only be considered in urgent cases or if you are in severe financial difficulty. If you urgently need to sell or move house, you will need your lender’s permission if the sale price is not enough to repay the mortgage.

The best thing to do is keep the home and continue paying the mortgage each month.

9. Proof of Marital Status

To get a marriage certificate you need to provide:

· Full names before marriage

· Date of marriage

· Name and full address of church, civil registration office or venue where the marriage took place

· Fees

A marriage certificate costs€20.

Postage for online and postal orders is €1.50 per order in Ireland and €2 per order outside of Ireland.

You can order and pay by phone in most civil registration services.

Some civil registration services have a walk-in service.

Phone orders are usually processed in 5 working days.

10. Planning Permission Documentation

To sell a house/apartment you must be able to prove that the property was built incompliance with planning permission and designed and built-in compliance with the Building Regulations. Proof is by a certificate from a qualified architect or engineer. If you have built a small extension this may be exempt but even so, a certificate confirming this will be required.

In addition to planning permission, any development will also generally need to be compliant with building regulations.

A certificate of compliance is a certificate issued by a properly qualified building Surveyor confirming that the property is built in accordance with any planning permission granted. If there are differences between the property and the planning, the surveyor will need to confirm that these differences are indeed exempt development, and the certificate will be qualified to cover this.

It really is best practice to obtain planning permission for all alterations whether they may be exempt or not –this ensures that your property is fully compliant with all aspects of planning, including building regulations, and will avoid any last-minute hitches.

My advice would be to IMMEDIATELY have the property inspected by a qualified building surveyor, or similar, with an instruction to him to issue a certificate of compliance. This will very quickly establish the necessity for any planning application for retention that may be required.

11. PPS Numbers

Irish Tax Numbers (PPS Numbers)are required by all Vendors and Purchasers to sell or purchase property in Ireland irrespective of whether they are resident for tax purposes in Ireland or not. The PPS Numbers are required to stamp the Deed of Transfer/Indenture of Conveyance for Stamp Duty purposes.

12. Principal Private Residence Declaration

A Principal Private Residence (PPR)is a house or apartment which you own and occupy as your only, or main residence. You will be exempt from CGT if you dispose of a property that for the entire period of ownership, you:

· lived in it as your main residence

· used all the property as your home

· Restrictions apply if only part of your property was used as a home.

You can only claim for the part of the house you used as your home. For example, you might have used half your house as your home, and half for your business. You can claim exemption on half of the chargeable gain.

The Rent-a-Room scheme will not affect your claim for full exemption.

Restrictions apply if you have not always lived in the property.

You can only claim for the time you lived in the property.

Absences considered as living in the property

You will be considered to have lived in your property where:

· you could not live in the property because your employer required you to live elsewhere (up to a four-year maximum.)

· you had a job, all the duties of which were performed outside the Republic of Ireland

· your PPR remained unoccupied, and you were either:

o receiving care in a hospital, nursing home or convalescent home

o resident in a retirement home on a fee-paying basis.

13.If your home is an apartment, you will need to provide Hogan Estates with a copy of the current Service Charges Budget, and the amount currently in the Sinking fund.

How management fees (service charges) are calculated

In general, the developer sets out the initial calculation method for management fees and sinking fund contributions. The calculation method should be set out in the contract to buy your property. The initial fee is usually set out in your contract, but the management fee for the following years won’t be known in advance and may change.

What happens if you don’t pay your management fees?

As a property owner, you would have signed a contract or lease when you bought your property which means you are legally obliged to pay your management fees. If you do not pay, the OMC (Owners Management Company) can take legal action against you. Any outstanding debts you have to the OMC can be tied to your property.

Sinking Fund

A sinking fund is a pot of money that is put aside every year to cover the cost of major long-term expenses. The Multi-Unit Developments Act 2011 introduced a legal requirement for OMC (Owner’s Management Company) to establish and maintain a sinking fund.

The Multi-Unit Developments Act 2011 requires that the amount of €200 per unit must be paid into a sinking fund every year, however this amount can be higher or lower once the amount to be paid is agreed by a meeting of the members. The sinking fund is for longer term expenses, such as lift or roof replacement or repair. The Multi-Unit Developments Act 2011 states that a sinking fund is to be used for refurbishment, improvement or once-off maintenance, or advice from a qualified person in relation to these types of work. It is a legal requirement that money in the sinking fund must be held in a separate account from management fees and the authorisation of the Directors of the OMC is required to access the sinking fund.